Is the feeding frenzy OVER?!? Not quite, but it seems to be a LOT better? Of course that is relative! and in this case I mean relative to the crazy times we were in in March – May!

In this video and blog post I’m giving you the current conditions of the market for the 7 county Twin Cities area broken down by property type and then I’ll go into a bit about what we see as far as what terms are resulting in accepted offers right now. These are the encouraging signs I’ve been looking for!

This year has definitely been one for the books! It has been the strongest sellers market that anyone I know can remember – and this is AMAZING if you have a home to SELL! Prices are higher than ever and you can dictate the terms for the MOST part – HOWEVER! Buyers! Do not despair! Things ARE getting easier for you now (at least compared to a couple of months ago when it was an all out SCRUM!)

A note about these graphs – I chose to make them show monthly ups and downs without the smoothing effect that softens the seasonal aspects, so keep that in mind as you look at the dips and heights. the market changes constantly, and this shows those changes month to month.

The median SFH price in the Twin Cities sits at $380,000 – that is UP from $326,100 at the beginning of this year.

You’ll often hear me talk about the “absorption rate” or the # of months supply of housing available to be sold if no other homes were to go on the market. For context it is considered a BALANCED market if there is 5-6 months of supply. We have been UNDER 1 month for different segments of the market for much of this year, mainly anything under about about $600K. Right now we are STILL at .8 months for anything under about $400k. For single family homes in general we are at a little over 1 month’s supply of homes.

Homes are only on the market for FIVE DAYS!!! a year and a half ago it was FOURTY FIVE! And only 6 months ago around 20! So still homes are still flying off the market.

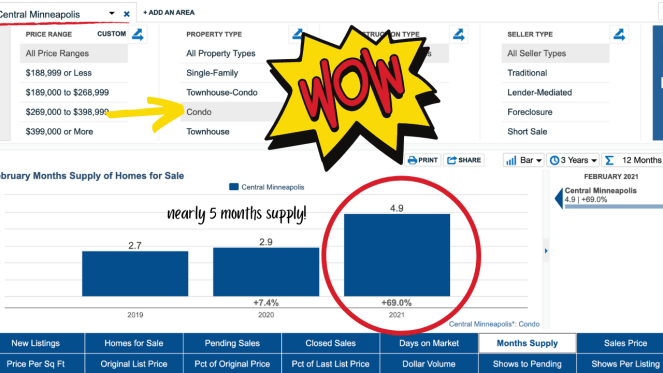

Let’s look at the 2 softer spots – Townhomes and Condos.

The median price for a townhome is consistent with the rest of the market rise in prices and is at $271,000 from $240,000 in January.

For Townhomes there is a little uptick in supply and we have a full month available right now.

Condos! This is the place if you’re looking for any kind of deal! Sellers are negotiating! You can get an INSPECTION! 🙂

Condo prices are at $171,000 for a median price, up a similar amount from the beginning of the year as other property types are.

The supply of condos is where the opportunity comes in – Still a sellers market but for people selling condos it can feel like a whole different world. There are 2.5 months worth of inventory available. This has dropped a small amount since January but has been relatively flat this year overall.

Now let’s look at what kinds of offers are being accepted!

This is a valuable bit of information that the Minnesota Transaction Coordinators gives us on a regular basis and I’ll add my 2 cents to about what I am seeing (although as a much smaller segment of the market)

Offer Acceptance Rate: 42%

Inspections Waived: 31% – we haven’t been in the 30% range since March

My 2 cents: the last 6 contracts (this past month or so) that I have either written or accepted have had inspections included and accepted. that’s 100% of my sales in the past several weeks. I’ve been thrilled for my buyers and I am 100% fine with it for my seller as well because I feel like inspections protect EVERYONE, the buyer, the seller and ME.

Pre-market Sales that happen without hitting the MLS : 2.8%. This is DOWN from earlier this year! It was over 5% for quite a while – maybe due to pandemic fears about having too many people in a home?

Average Purchase to List Price: 102.7% – about the lowest it’s been since the spring market!

Still great for sellers, but also good news for buyers! And a lesson to sellers about pricing appropriately. Things change, you want to not have YOUR home sit because it’s been priced too high as well as understanding that unless you have something really special that the insane bidding wars may be over for now.

I have talked to many agents saying that showings are down from earlier this spring when agents were setting overlapping showings and having the home packed full of people for 12 hours per day. Now there are private showings again. There may be open spaces in the calendar. More than one offer may come in but they aren’t seeing the literal STACKS of offers that they were before.

Financing Types:

Cash 11.5%, which is higher than it’s been

Conventional 68.5%, – a little lower than its been

FHA 8.5%, higher!

VA 3%, Still a rough spot! People that use VA are often choosing it because it is a no downpayment loan, which means they are short on cash. If you can’t make appraisal gap guarantees, or add other sweeteners that need ready cash available this can be a VERY tough time to buy.

USDA 8.5% (this is a high number and I wonder if it is a function of the sample size that they had – if they had 2 transactions it could hit this #). These loans are generally for rural buyers.

Seller Paid Closing Costs: are at 12%

Home Warranties: 5.7% – I was able to negotiate this recently as well!

Contingent Upon the Sale of the Buyer’s Property: 8.5% (this seems HIGH to me! I’m still cautious about having this particular contingency, it can be a real weak spot in an offer if you have any competition at all. I would avoid this at all costs or you may have to make it an offer they can’t refuse due to price, or magically find a seller that wants to stay a little longer.

And that is ALL for this week. I’ll be back next week with some more neighborhood profiles. I’ve been AWOL due to this insane market and actually getting a vacation for the first time in YEARS. No regrets. 😉

See you then!