When most people hear “Minnetonka,” they immediately think expensive homes, lake life, and luxury neighborhoods—and honestly, that reputation is well earned. With top-rated schools, mature wooded lots, proximity to Minneapolis and MSP Airport, and easy access to Lake Minnetonka, the Minnesota Landscape Arboretum, regional parks, and apple orchards, Minnetonka is one of the most desirable suburbs in the Twin Cities.

Right now, the average resale home price in Minnetonka is around $718,000, and new construction is closer to $740,000 or more if you can even find it. So when I recently started showing homes in a pocket of Minnetonka where prices are still in the low $600,000s, I was genuinely impressed.

A Retro-Built Neighborhood That Lives Large

Most of the homes in this more affordable section of Minnetonka were built in the 1970s and 1980s. And while that era might not sound glamorous at first, these homes have something many modern builds simply don’t: actual rooms.

Instead of one massive open-concept floor plan, these houses typically offer:

4 or more bedrooms

Separate family rooms and living rooms

Kitchens that don’t dominate the entire main level

Flexible spaces perfect for offices, playrooms, or quiet retreats

If you enjoy gathering as a family—but also value the ability to close a door and not stare at the kitchen mess—this style of home just makes sense.

Big Lots, Hills, and Mature Trees

What truly sets this pocket apart is the land.

Many of these properties sit on ½ acre or more, with:

Rolling terrain

Curving neighborhood streets

Towering mature trees

A peaceful, established feel

You’ll find this housing style throughout the Twin Cities, but the combination of lot size, price point, and location is what makes this area particularly special.

Easy Commute & Everyday Convenience

Another major perk? Location.

From this area of Minnetonka, you’re about:

20 minutes to downtown Minneapolis

20 minutes to MSP Airport

Minutes from Target, Cub Foods, and Ridgedale Center

Close to all the restaurants, small shops, and local charm of downtown Hopkins

That’s a rare mix of space and convenience that’s becoming harder and harder to find.

Who This Area Is Perfect For

This neighborhood is ideal if you’re looking for:

A retro home with character

Large yards for kids or dogs

A quiet suburban feel

Short, manageable commutes

And a price that’s below the Minnetonka median

Minnetonka doesn’t usually scream “affordable,” but this hidden pocket proves that great opportunities still exist if you know where to look.

If you’re searching for a home in Minnetonka or anywhere in the Twin Cities and want help finding the smartest value for your budget, I’d love to help. I’m Mary Schumann, a Minnesota relocation specialist, and I help buyers move smart in Minnesota every day.

If you’ve ever contacted a real estate agent because you loved their marketing, their videos, or their personality… only to suddenly find yourself working with someone entirely different, you’re not alone.

This is one of the most common complaints I hear from buyers and sellers relocating to — or moving within — the Twin Cities. They thought they were hiring that agent, but instead they got handed off to someone on their team. Often, it’s a newer agent still gaining experience.

So let’s talk about it: Should you work with a solo agent or a real estate team? And what does that experience actually feel like as a client?

As a solo Twin Cities Realtor who handles every part of the process myself, I’ll tell you what you can expect — and why this choice matters more than most buyers and sellers realize.

What Really Happens When You Hire a Real Estate Team

Real estate teams are built for one thing: volume. The larger the team, the more clients they can run through the system. That’s great for them… not always great for you.

Here’s the typical experience:

You reach out to “Top Agent Jane,” the one all over YouTube and Instagram.

Jane doesn’t personally take new buyer calls.

Your information goes to their “buyer specialist” — a newer agent learning on the job.

That buyer agent might not have the negotiation experience you expected.

The lead agent may never show up at a showing, a strategy call, or even your closing.

There’s nothing wrong with new agents — everyone starts somewhere! But you didn’t choose that person. You chose the face of the brand… and got someone else.

For many people, this feels like a bait-and-switch — even if it wasn’t intentional.

What It’s Like to Work With a Solo Agent

When you work with a solo agent, the experience is entirely different.

You get the person you contacted. Every step of the way.

I know your timeline. I know your story. I know your preferences, your deal-breakers, your stress points, and your goals.

And because I’m the one taking every call, attending every showing, writing every offer, and negotiating every term, nothing gets lost in translation.

There is no hand-off. No “let me check with the team.” No confusion about who’s managing what.

Just one dedicated professional who truly knows your transaction from the inside out.

Why Experience Matters — Especially in Negotiation

One of the biggest advantages of working with a seasoned solo agent is negotiation skill.

Many team-based agents specialize only in buyers or only in sellers. That sounds good… until you realize they don’t understand what motivates the other side.

When your agent works with both buyers and sellers — and manages every part of the deal personally — they have a complete understanding of:

how sellers evaluate offers

what buyers notice (and what they don’t)

how listing agents prioritize communication

what makes an offer stand out

what terms truly matter in today’s Twin Cities market

You get strategy, not just logistics.

A Solo Agent Learns YOU — Not Just Your File

Real estate is deeply personal. Buying or selling a home is emotional, stressful, exciting, and sometimes overwhelming.

When you’re passed between team members, the experience can start to feel transactional.

When you work with one dedicated agent, you get something simpler and more meaningful: trust.

You don’t have to re-explain yourself. You don’t have to wonder who’s calling. You don’t have to worry that someone new has taken over your file.

Instead, you get consistency, clarity, and confidence.

So… Team or Solo? What Should You Choose?

Real estate teams work well for highly structured, high-volume business models. Some consumers prefer that.

But if you value:

✔ personal communication ✔ consistent guidance ✔ a seasoned professional overseeing everything ✔ relationship over volume ✔ thoughtful, strategic, experience-based advice

…then a solo agent might be exactly what you’re looking for.

And if you’re relocating to Minnesota — or moving within Minneapolis/St. Paul — having one dedicated guide makes the process so much easier.

And if thinking twice doesn’t do it, think a few more times—because you may be buying a house you’ll be stuck with for a LONG time.

I’m Mary Schumann, a realtor in the Minneapolis area. I help a LOT of buyers find the right home here. I’ve seen horror stories, analyzed inspection reports, and run the data on enough houses to confidently tell you to stay away from the following types of homes. Some of these tips may seem like common sense, but circumstances can sometimes push buyers to overlook red flags. Don’t be that buyer!

1. Homes With Obvious Flaws or Hazards

If a home has an obvious flaw that can’t be fixed—STOP and reconsider. Examples include:

Located on a busy street

Backing up to a railway

Next to a run-down mobile home park

The number one rule in real estate is location, location, location. If you buy in a noisy or undesirable area, you’ll limit your resale options significantly. Busy streets, railways, and unattractive neighbors often scare off buyers with kids or pets.

Pro Tip: It’s often better to buy the worst home in the best neighborhood than the best home in a questionable location.

2. Homes Without Basements

In Minnesota, basements are essential. We get tornadoes here, and having a safe place to go during severe weather is key. Basements also provide:

Extra storage

Space for a family room or workout area

Most buyers expect a basement, so skipping one could hurt your property value.

3. Homes With Water Problems

Watch out for homes at the bottom of a slope or in flood zones. These can lead to:

Damp basements

Water damage and mold

Look for signs of water staining or dampness, and make sure the home has a sump pump—a good sign the seller has mitigated any water issues.

Flood Zones Tip: Minnesota does well with water management, but always check flood maps if you’re near rivers or creeks.

4. Homes With Steep or Long Driveways

Minnesota winters mean snow and ice—and neither is fun on a steep or long driveway. Problems include:

Cars getting stuck or scraping low-clearance vehicles

Slipping on ice when walking up or down

Sunlight Tip: Driveways facing south or west get more sun, which helps melt ice and snow faster.

5. Poor-Quality New Construction Homes

Don’t get distracted by fancy finishes like granite countertops. Instead, focus on:

Durability of floors and carpet padding

High-quality mechanicals (furnace, AC, etc.)

Reputable builders with strong reviews

Minnesota has a 1-2-10 warranty on new construction:

1 year: Full coverage

2 years: Mechanical systems

10 years: Structural defects

Get a home inspection in the 11th month of your warranty to catch issues early.

6. Older Homes With Bad Roofs

Insurance companies may refuse coverage if a roof is in poor condition. Always check roof age and quality before buying an older home.

7. Homes at Dangerous Intersections or Curves

Avoid homes on T-intersections or tight curves. These locations often:

Attract traffic accidents

Shine headlights into your windows at night

8. Homes With HOA Restrictions

While Minnesota’s HOA rules are often less strict than other states, review them carefully. Minnesota law gives buyers a 10-day review period for HOA documents, including:

Rules and regulations

Budgets and expenditures

You can cancel your offer and get your earnest money refunded during this period if you don’t like what you see.

Final Advice: Don’t Skip Inspections

Yes, inspections are expensive, but they can save you from making costly mistakes. A high-quality inspector can uncover issues you may not be able to negotiate or fix later.

Work With a Realtor Who Tells It Like It Is

Thinking about buying a home? Find an agent who gives you honest guidance. My role is to arm you with the information you need to make smart decisions.

If you have questions, reach out! I love hearing from people who find me on online or on YouTube.

What is happening in the Minneapolis area real estate market? I’ve been following several metrics over the past few years and there are a few that really stand out to me as indicative of how the market is doing, not just PRICE but what kinds of terms are included in winning offers and I will let you know which terms are revealing the current state of the market here.

I’m keeping my finger on the pulse of what is happening in the Twin Cities metro real estate market so you can be an informed buyer or seller.

The number one question that most people have about homes is whether or not prices are falling? I keep hearing this and for the purposes of this discussion I’m just going to look at the 7 county metro around Minneapolis and St. Paul and we can check the different housing types. The first is the most popular -SINGLE FAMILY HOMES. When I was digging into data for this update I decided to look at it over the past year and the past 10 years so that I can show you trend lines for both. I’m also going to differentiate by new construction and previously owned because new construction is at a vastly different price point as a whole.

Prices & time on market for existing homes

Metrics that I didn’t talk about in the video are how long houses are staying on the market these days. I do see houses sitting for quite a long time in certain areas and price points but the official numbers are charted here. The graph gives the impression of a big increase in time, but real numbers equate to only 3 more days.

New Construction

I’ll talk about pricing but for new construction I see a lot of opportunity for buyers here! Why? Builders have a lot of inventory right now. They have completed homes as well as homes that are underway with completion dates coming up. They need to get these homes off their books so they can continue to build and the interest rates have slowed things down for everyone, but the big builders are offering rate buy downs for buyers right now along with all kinds of other incentives, from appliance packages to closing costs.

Things to consider are that these homes are mainly being built in 3rd ring suburbs and exurbs so if proximity to the city is important you’re less likely to be able to get a new build – or at least one with a big builder that can offer these incentives. There are custom builds on lots here and there in the city.

You’ll see a slight dip in median price ($5000) from the beginning of the year. I have read in multiple sources that they estimate that it would take 10 years of building for the builders to catch up to demand for homes due to the after effects of the housing recession in 2008. We are still that far behind. New construction is showing over 6 months worth of supply but take this with a grain of salt because builders list homes that are TO BE BUILT – so they aren’t existing yet – along with those that they have ready for a buyer to move into.

New construction supply shows a buyers market! I haven’t seen this kind of number in a VERY long time. Ever?

Things are different when you look at previously owned homes. It is still a sellers market, although not the insane sellers market of a year or 2 ago. Homes still get multiple offers, the market is still moving just not at a runaway pace. Previously owned single family homes are sitting at about 1.3 months supply. So you can see the difference here.

WHY is it a seller’s market for existing homes and a buyer’s market for new constructions?

What leads to this? 80% of people with a mortgage on their home are paying less than 5% interest, 50% of them have a rate at less than 4%, they need a big incentive to list their homes and buy a different home with a mortgage at a higher rate. This really is one of those cases where as usual, of you have a good budget you are at an advantage because you can buy new construction and take advantage of the market and the incentives whereas those 2 things don’t exist as much for existing homes, prices are lower as a median but supply is lower too and you don’t get the builder buy downs. But you also don’t have to pay for a deck or the multitude of finishing touches that need to be added to new construction.

Price reductions

Housing inventory is dropping now as we get into the winter and holiday time, but the other thing that is slowing is PRICE REDUCTIONS – the percentage of them is reduced by about half of what it was 1.5 to 2 months ago, from 14% of listings to about 7%. Maybe agents and sellers are pricing correctly now, or maybe they understand that they may spend more than 5 minutes on the market?

Bank owned homes

Another statistic of note are the number of distressed or bank owned properties. We still have fewer than 100 listed out of about 6200 active listings. Less than 1.5%, other markets in the US are not faring as well. People here are still meeting their mortgage payments.

Offer terms that show a big shift

OK – a couple of other things that really stand out to me – the first is that sellers are contributing to buyers closing costs 43% of the time! that’s the highest percentage I can remember seeing. People including appraisal gap language on there offers has almost disappeared (although escalation clauses are still being included) but this makes sense when you see that most sellers are now seeing themselves getting about 99-100% of asking – this number was at 105% or more for a while and that was just crazy. Another option if you are in the previously owned category of home, if you find one you like and it has a motivated seller you could ask for them to do the rate buy down for you. Interest rates have been dipping back down, but it’s doubtful that they will ever get as low as they were during the pandemic. This will likely spur some more buyer activity as we head into spring.

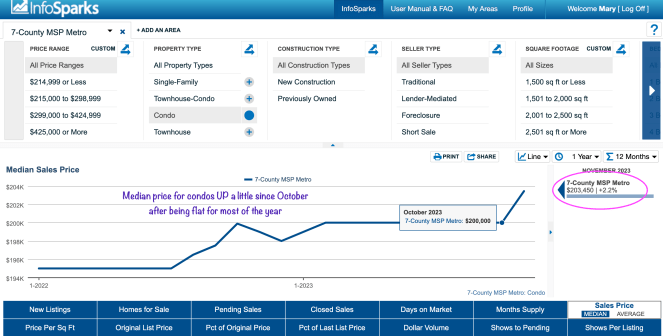

Data on Condos and Townhomes

If you have questions about the real estate market in the Twin Cities area – city or suburbs! – reach out! I love to talk to people that meet me YouTube or the Blog! Mary

You’re not helpless when it comes to mortgage interest rates! A lot of buyers are concerned about monthly payments now that the interest rates have gone up.

I talked with Chris O’Connell at Loan Depot about 4 options that home buyers have to pay a lower interest rate and therefore a lower monthly mortgage payment. Chris had one that was surprising to me and we talked a bit about the one that seems to be getting a lot of attention in the real estate world right now, the 2/1 buy down and why that may not be the BEST option.

Take a look at this video interview if that is something that is worrying you as you think about buying a house now.

I specialize in helping people relocate to MN from other parts of the United States and the world thanks to people finding me on my YouTube channel. It’s a niche that I love to serve, people are choosing Minnesota and I love to welcome them here.

I know that this can be a difficult thing to do – uprooting your life to make a change to a completely different everything! The climate, the people, the way that Minnesotans live – which is very much OUTDOORS. Many people make the choice for that very reason. One of the other themes that I hear often is affordability and high quality of life.

If you’re curious about the perspective of this couple, what things felt like challenges, how they overcame those, what made them choose MN, what surprised them when they got here and what they have enjoyed so far, you’ll probably enjoy this video!

If this is a move you are considering making and you have questions please don’t hesitate to ask! It’s what I do day in and day out. 🙂

I went out and looked at some of the homes on the Parade of Homes tour and this custom build was so pretty. Click to watch my tour with the listing agent. It was a truly grim day on the outside, but bright and comfortable inside!

Does the phrase “appraisal gap” strike terror in your heart? Or leave you scratching your head? What about hearing tales of “appraisal guarantees” that are often needed when you’re a buyer in this seller’s market? If you’re a buyer or seller and you’re not spending every waking (and sleeping!) moment thinking about the real estate market, you may be confused about what these terms mean for you, and they may feel a little scary. Knowledge is power, so let’s talk about what an “appraisal gap” is and what an “appraisal guarantee” means for a buyer or a seller.

If you’ve watched any of my market update videos you’ve heard one thing reiterated and that is that we are in a historically strong sellers market. We have a lot of buyers competing for every home and that means that we nearly always have multiple offers and those offers are often for well over list price as buyers do whatever they can to beat the competition.

On the surface you may wonder “how can that be a problem”? if you’re paying with CASH it’s not a problem, you can pay any price you choose to pay for something as long as you can show that you have the funds available to do it. This is a big reason why cash buyers have an advantage right now, the price is the price and the seller doesn’t have to worry about the bank’s appraised value.

However 80+% of people are NOT cash buyers, they have to get a mortgage for their home purchase and as part of that loan the bank will hire an independent appraiser to look at the property and determine if it’s worth the amount they are loaning you for it. They don’t want to be stuck with worthless collateral to sell if you default on your loan. This evaluation of value is called an “appraisal”.

Sometimes your mortgage lender’s appraiser says the house IS worth less than you agreed to pay. This is known as an appraisal gap or a low appraisal.

I sometimes hear buyers with high loan approval amounts suggest that it might be a good strategy to buy a lower priced home and just throw a large amount of money at it because they can qualify for a loan of that size, but that still doesn’t eliminate the issues around homes appraising for the value of the loan. And really, appraisals exist for this very reason.

Options as a buyer

What are your options as the buyer if you’re worried that the appraisal will come in lower than what you have offered? after all – Sellers want to get the price you’ve offered in the contract whether or not the appraiser says it’s worth that amount as loan collateral.

The option that has been most successful with sellers is writing appraisal gap coverage or an appraisal guarantee into the contract for the purchase of the house. We are seeing this happen about 45% of the time now and it is getting to be more common as the market continues to be tight.

What this essentially means is that you will put a larger down payment on the home which bridges the gap between what you’ve offered and what the bank is willing to loan and preserves your ability to finance the purchase and close on the home.

A typical home purchase contract has an appraisal contingency: wording that says the buyer can call off the deal if the property appraises for lower than the buyer offered. But in hot real estate markets, where buyers outnumber sellers, some buyers waive the appraisal contingency. These buyers either pay cash for the home or gamble that they have money to pay the difference between the appraised value and the price, however much that may be.

rather than waiving the Appraisal contingency entirely, offering to cover the gap on a low appriasal is the middle path. You’re offering some amount that you will make up via a larger down payment.

Take the example of the $120,000 offer on the $100,000 home that has a $10,000 difference between the purchase price and the appraised value:

If you had offered to cover an appraisal gap up to $10,000, you would proceed with the purchase, bringing that extra $10,000 as a larger down payment.

If you had offered to cover an appraisal gap up to $5,000, you would be entitled to withdraw your offer and get your earnest money deposit back. That’s because the difference between the offered price and the appraised value is greater than the $5,000 appraisal gap coverage.

At this point, the seller may wish to negotiate with you to keep the transaction in tact and they may agree to lower the price by the remaining $5000.00 difference, or they may choose to go to the next buyer.

You’re more likely to succeed when offering appraisal gap coverage if you include proof of funds to do this as well.

If you’re lucky, you may not have to worry about appraisal at all. The bank may waive the required appraisal if they can see market conditions support it and that the buyer is bringing 20% or more as the down payment. This means that they look at the market data and determine that the property is likely worth the purchase price, but you will not know this until you’re closer to closing.

Things to think about

A couple of things to add as you consider whether or not to do this on your next purchase agreement:

Think about the home you’re buying, it’s condition, price, and location and what you’re willing to do to purchase that home. You want to be doing this for a home that will hold or appreciate in value.

Because of the market conditions, home prices nationally increased over 14% year over year. Median home prices in Minneapolis and the Twin cities went up 10.9% year over year according to the Minneapolis Area Association of Realtors.

Put that into perspective with your purchase.

If you are buying a home priced at $100,000 today and prices continue on their current path, that home would be valued at $111,000 a year from now.

If you’ve agreed to make up $5000, or $10,000 in low appraisal, the likelihood that you will be “whole” in a short period of time is there.

Another consideration is whether or not you will be able to afford a home in a year or two if this continues and if interest rates continue to rise.

So, it’s a math problem. Never been a big fan of math problems, but looking at it this way really adds some clarity and perspective.

Reach out with questions! I’m always happy to help.

A month goes by in a hurry it seems, so here we are! Did a month make a difference with the real estate market? YES. It is notably busier!

Click here to watch. 🙂

I don’t think I’m telling you anything you don’t already know, but the real estate market is on fire. Someone hit the gas pedal on the housing market in February and they have a lead foot. What does this mean specifically? Let’s look at the twin cities housing market as of Feb 18 2022.

If you are a seller – LIST NOW and you’ll be partying all the way to the bank.

Just about every listing is getting multiple offers in the first couple of days. The supply of buyers is so great and the supply of homes is so low right now – 15% fewer listings on the market than last year at this point!

Why are sellers hesitating? I assume that it’s because they are worried about finding THEIR next home. As an agent that represents a lot of buyers, I can tell you that sellers can not only command great prices for their homes they can still get a closing date that suits their needs. For example, if a seller is considering putting their home on the market, but are worried it will be gone in a blink, there is a great likelihood that the seller can ask for and receive a 60 close, flexible closing, or recently I’ve seen them asking for a seller’s home purchase contingency or lastly a rent back situation after closing remembering that most conventional loans require the transaction to close in 60 days on the buy side so no long term rentals this way! but this way the seller will have cash in hand and be able to buy while also have a roof over their heads while they wait for their next home to be available.

One of the things that I really like about real estate is that EVERYTHING is negotiable – as long as the parties work it out (within the law!) and get it in a signed contract, the parties can work together to find a solution that works for everyone. Do you have a creative way to structure a contract that lets everyone get what they need? Bring it up and there may be a way to make it work out!

This past week we had offer acceptance rates at 15%, which means that sellers are receiving 6-7 offers on average. But the average for the month is hovering around 35% according to Home Free Transaction Coordinators. I’ll give you more info on what they see in a successful offer after I take you through current market conditions.

Absorption rate

It’s a seller’s market, but to what degree? In the past I’ve explained that the way that we determine this is based on the absorption rate or how many months worth of housing inventory we have at a given time if nothing new were added to the market. 5-6 months is considered balanced, more than that is a buyer’s market and less is a seller’s market. Obviously the more extreme the number the more it favors one or the other. That obviously varies by housing type.

Single family homes have a .56 months (about 17 days) supply now as compared to one year ago when they were at .62 (about 19 days). We have started this year off with available inventory down by 21% year over year. New listings this month are down by 15% from last year.

I was looking for a bright spot and looked at new construction. Builders are responding to the need for houses and have started increasing their production too.

This image shows the big dip and now the increase starting in single family new builds between $400 & $600K. Its not dramatic, but any amount helps – if you have 50 more houses that’s 50 buyers that have found something.

If you have been thinking about selling and are curious about what your home is worth today, let me know. I’ll give you a free estimate of what your home is worth today – absolutely no obligation, just for your information if you want to know – just send me an email. We need homes and now is definitely the time to get the maximum amount of money out of your sale! mschumann@kw.com if you’re curious. I’m happy to do it.

Townhouse/ Condo properties are at .97 months (29 days) vs 1.13 a year ago (34 days). Prices on Townhouses are at a median of $267,000 which is UP 12.2%. Average days on market for a townhouse is down 26% to 14.

Condo prices are at a median of $195,000 up 6.6% from last year and are on the market for about 30 days. If you are a first time buyer or someone that likes condo living, this is the softest spot in the market today and your biggest opportunity.

Single family homes in the 14 county metro area have a median price of $370,000, a gain of 12.1% year over year. They are on the market for NINE DAYS. Only about half of what we saw a year ago. And don’t fool yourself thinking you have 9 days to think about it, this is a listing going live on a Thursday, showing through the weekend, closing offers on Sunday and allowing a 5 day inspection period before heading to pending.

The combined absorption rate (all property types) is at .67 months or 20 days of inventory as opposed to one year ago when we had a whopping .75 months or 22 days of inventory.

What can you do if you’re a buyer?

Here are my suggestions and strategies:

1.my office posts properties to agents internally that are off market and that sellers are willing to part with before going onto the MLS, so having that network available helps a lot!

2. make sure you see what is available in “coming soon” and get in there quickly

3. even better if you have the nerve- offer “sight unseen” while in this status. if the seller will do it, you can usually negotiate an inspection this way and if there is something wrong with the property get out of the contract without losing your earnest money, this does require a good offer out the gate. It’s not a way to get a bargain, but is a way to quit losing in multiples.

4. make your offer more appealing are to offer appraisal gap coverage. This means that if you are financing you are stating that you have the ability to make a larger downpayment in order to cover the gap between your offer and what the bank is willing to loan you, having cash is a very important piece of the puzzle in this environment. You can offer any amount of appraisal gap coverage – it doesn’t have to be 100% of the difference!

5 Look at “wallflowers” these are properties that have been on the market for longer than 4 days. This means they have made it through a weekend without getting an offer and may be more willing to negotiate or look at a reasonable but not extreme offer. These can be homes that a buyer got cold feet on, that their financing fell through or other scenarios.

6. Don’t ignore properties that need work! You can get a home loan that rolls a remodel into it. Not everyone can look past a dirty unfinished basement but it’s rarely a bad investment to add finished square footage to a house – especially in an in demand neighborhood.

7. Do you have time? Offer on new construction. You eliminate multiple offers and choose your finishes. Just be aware that contracts allow builders to cancel your contract if the price of materials goes up and you can’t cover the increase. Don’t get yourself in too deep.

8. There aren’t a ton of these available but spec houses are a good option. They may be completed new builds OR they may be nearly completed with an estimated move in date already.

9. my last option coming to mind to look at loans that allow you to offer as if you’re offering CASH – without a financing contingency. This seems like a HUH??! moment, but in my video next week I’ll interview a lender with a program like this that may give you a leg up and I’ll post it here, of course!

Accepted offers

OK – lets look at what’s been going on with offers per HFTC:

Buyers are waiving inspection 46% of the time, this is a lot, but that also means that 54% of the time they are getting an inspection.

Off market sales are at 12% – this is the “private listing network” that I mentioned where agents that have upcoming listings market them internally first.

Sales Contingent on the sale of the buyer’s home is down to 5% of the time.

Average sale to list price is 103.2%. I don’t know where these are happening because my buyers have been offering at 15% over and losing… We would be happy with 103%!

Cash is at 17% of offers, Conventional at 69%, FHA has ticked up to 5%, VA is at 0.

Hey! I would love to hear from you in a comment or an email or a smoke signal … reach out if you have questions!

Hi and happy new year! Who wants to start the year off with some DATA and a look at what the real estate market is doing PLUS what I believe will happen with the housing market in 2022? I actually LOVE data – it tells a very clear story, so let’s dive in and take a look at what that data is telling us.

Prefer to watch rather than read this? 😉

I wish I had a crystal ball to tell you what is going to happen to the real estate market in 2022, I don’t, but I will make some educated guesses! In addition to that I’m going to share with you what the offers that have been accepted have looked like in the past month.

I like that info because it is ALSO a gauge for how strong the market is – what are sellers wanting to see and what are buyers willing to do to win?

Sisyphus at work

in 2021, being a buyer (or a buyer’s agent!) could feel like pushing a boulder up hill. It was hard, tiring, a little stressful but it was ultimately satisfying if everyone hung in there (I’m stubborn – I don’t quit).

It’s me. I’m stubborn like a mule.

The market was really rough for buyers because demand for homes here is HIGH and supply is LOW. I think many of us went into this winter hoping for a bit of a break on the horizon, but the numbers are not making it look like that will be the case.

Inventory of homes was really low LAST January first – historically low! and as of the first week of january this year we have 15% fewer listings on the market to choose from than we did then. We are still in a ridiculously strong seller’s market.

Fun fact – the last time the market was considered “balanced” in the twin cities was 10 years ago. It has favored sellers ever since and doesn’t seem to be lightening up at all.

As a colleague said today, there is a lot of national press saying that the market is loosening up but the numbers tell a different story.

Do tell, National News!

It’s important to look at DATA for the market you’re in and understand what that means for your situation. So let’s look at the data for the twin cities – you know that price is a function of supply and demand, and we have already established that supply is low. It has been consistently low for years and the recent challenges with supply chain and lumber prices are not helping supply to correct that quickly. It’s going to be a long term process.

Absorption Rate

Realtors look at how many months supply we have of homes available to sell if NO OTHER HOMES ARE LISTED in order to determine what kind of market we are in – 5-6 months is considered a balanced market, fewer months worth of inventory favor sellers and the smaller the number of months the more strongly it favors them, and vice versa for buyers.

Currently, the total months supply we have now including ALL property types is 8/10 of one month. .8 months is WAAAAAY less than 5-6 months.

If you break this down further you see that single family homes are at .7 months supply this year (one year ago we had 9/10’s of a month), Condos have been the softer spot and currently have a 1.6mo supply down significantly from a year ago when we had 2.8 months, and townhomes are just like single family homes with .7 now vs .9 a year ago.

An interesting thing to me is that high end homes are seeing the market tighten up a lot now too. That area had more wiggle room last year, but it looks like that is no longer the case.

Broken down by price point

Median price by property type

If we take a look at prices we see what this high demand has done over the course of a year, single family homes are at a median price of $360,000 UP 10% year over year from $326,300 (emphasizing that this is a MEDIAN price for the entire metro area, obviously prices range widely!)

Townhomes show a similar increase of 8% from $240,000 a year ago to $259,900 now.

Condos despite being the soft spot ALSO rose in price – they are at $191,000 up 11.6% from $171,000 a year ago.

Demand side of the equation

The other side of the equation is DEMAND. What leads to this high demand?

A couple of things that I can think of the first of which are the low interest rates. The Fed is talking about raising them this year but even if they do, these changes are typically incremental as they test to see the effect on the markets for everything – not JUST homes.

If the rates rise a bit – even to 4%? will that tamp down the demand for homes?

I personally don’t think it will have an enormous effect, the demand is so high, and even 4% or 5% are STILL low interest rates. In the past I have paid interest at 8.25% for my first home, 6.5% for my second, we paid 4% and thought we had a steal when we moved to MN! Yes, we refinanced when the rates dipped again, but you get my point. It’s relative, and people want a place to live that belongs to THEM and gives them essentially rent control and a predictable expense PLUS the joys of having your own home.

The second factor in demand is the fact that a very large bubble of millenials is aging into a time when they want to do the things that people do in early adulthood – get married, have a family, BUY A HOUSE. This bubble, or boom, is driving demand for homes.

Tips for BUYERS

If you are thinking of selling, your property will likely get scooped up VERY quickly this year. If you are thinking of jumping into the pool to BUY, I have some advice:

1. Understand that you are going to be in a difficult situation, you aren’t the only one looking at a house and if you decide to offer on it you will be competing with many other people. Do your best.

2.) steal yourself for the process. If you don’t get the first home you offer on, it will likely hurt a bit, get back in the saddle and try again. SOMEONE wins every one of those multiple offer situations – that someone CAN be you. You just need to have the chops to hang in there and keep swinging. If I’m working with you, I’m going to have your back every step of the way and help you present your offer in a way that makes the seller say – YES – that one!

3.) very important! Look at homes listed UNDER your max price. Almost NOTHING goes for list price right now, so you need to put yourself in a position of being able to offer over list.

4.) A corollary to #3 is that you should save as much cash as possible so that you have that wiggle room to cover appraisal gaps or increase a budget and put a smaller percentage down if you need to.

5.) lastly, don’t stop looking at the times when everyone else has stopped looking! If it’s a holiday or WINTER, now is a good time to look because you are competing with fewer buyers even if the supply is lower, too. I love to look on holiday weekends – sign me up for Memorial Day! I’ve not really had a break over the Christmas season this year because listings are selling now as well as buyers getting homes while everyone else is hung over from too much egg nog. STAY IN THE GAME. Take advantage of the situation.

Offers that are getting accepted NOW

Let’s look at what types of offers are getting accepted right now according to Home Free Transaction Coordinators – what are sellers looking for and buyers offering in the effort to get a home?

Offer Acceptance Rate: 52% this indicates multiple offers to me. We have been quite low on this in the recent past – under 30%

Inspections were Waived 30% of the time – summer was over 50%, now seems like a good time to buy if you REALLY want an inspection

Pre-MLS Sales: 4.4%, these are sales that happen off market, private network of agents marketing them to each other.

Average Purchase to List Price is the lowest I’ve seen this year at 100.87%, this was up around 105% in summer!

Financing Types:

Cash 19% – this is the highest I’ve seen and I can say that it reflects my own personal experience recently.

Conventional loans 73% – still the big daddy, and always will be.

FHA 2% still tough to get these accepted and that kind of stinks, but when you’re going up against cash, I can’t blame a seller.

VA 4% this is the highest I have seen in a year at least.

USDA 1%,

Other 1%

Seller contribution to Closing Costs: 37.8%, this can be in lieu of fixing something.

Home Warranties included in the sale 5.6%

Offers Contingent Upon the Sale of the Buyer’s Property are at 6.7% – this is actually DOWN quite a bit, I believe not too long ago it was around 10-12%. Try to avoid this of possible. It’s really tough to get accepted.

If you’re exploring communities, check out my neighborhoods and suburbs playlist on YouTube to take a look at different areas of the metro.

Let me know if you have questions or comments – love to hear from you!