What is happening in the Minneapolis area real estate market? I’ve been following several metrics over the past few years and there are a few that really stand out to me as indicative of how the market is doing, not just PRICE but what kinds of terms are included in winning offers and I will let you know which terms are revealing the current state of the market here.

I’m keeping my finger on the pulse of what is happening in the Twin Cities metro real estate market so you can be an informed buyer or seller.

The number one question that most people have about homes is whether or not prices are falling? I keep hearing this and for the purposes of this discussion I’m just going to look at the 7 county metro around Minneapolis and St. Paul and we can check the different housing types. The first is the most popular -SINGLE FAMILY HOMES. When I was digging into data for this update I decided to look at it over the past year and the past 10 years so that I can show you trend lines for both. I’m also going to differentiate by new construction and previously owned because new construction is at a vastly different price point as a whole.

Prices & time on market for existing homes

Metrics that I didn’t talk about in the video are how long houses are staying on the market these days. I do see houses sitting for quite a long time in certain areas and price points but the official numbers are charted here. The graph gives the impression of a big increase in time, but real numbers equate to only 3 more days.

New Construction

I’ll talk about pricing but for new construction I see a lot of opportunity for buyers here! Why? Builders have a lot of inventory right now. They have completed homes as well as homes that are underway with completion dates coming up. They need to get these homes off their books so they can continue to build and the interest rates have slowed things down for everyone, but the big builders are offering rate buy downs for buyers right now along with all kinds of other incentives, from appliance packages to closing costs.

Things to consider are that these homes are mainly being built in 3rd ring suburbs and exurbs so if proximity to the city is important you’re less likely to be able to get a new build – or at least one with a big builder that can offer these incentives. There are custom builds on lots here and there in the city.

You’ll see a slight dip in median price ($5000) from the beginning of the year. I have read in multiple sources that they estimate that it would take 10 years of building for the builders to catch up to demand for homes due to the after effects of the housing recession in 2008. We are still that far behind. New construction is showing over 6 months worth of supply but take this with a grain of salt because builders list homes that are TO BE BUILT – so they aren’t existing yet – along with those that they have ready for a buyer to move into.

New construction supply shows a buyers market! I haven’t seen this kind of number in a VERY long time. Ever?

Things are different when you look at previously owned homes. It is still a sellers market, although not the insane sellers market of a year or 2 ago. Homes still get multiple offers, the market is still moving just not at a runaway pace. Previously owned single family homes are sitting at about 1.3 months supply. So you can see the difference here.

WHY is it a seller’s market for existing homes and a buyer’s market for new constructions?

What leads to this? 80% of people with a mortgage on their home are paying less than 5% interest, 50% of them have a rate at less than 4%, they need a big incentive to list their homes and buy a different home with a mortgage at a higher rate. This really is one of those cases where as usual, of you have a good budget you are at an advantage because you can buy new construction and take advantage of the market and the incentives whereas those 2 things don’t exist as much for existing homes, prices are lower as a median but supply is lower too and you don’t get the builder buy downs. But you also don’t have to pay for a deck or the multitude of finishing touches that need to be added to new construction.

Price reductions

Housing inventory is dropping now as we get into the winter and holiday time, but the other thing that is slowing is PRICE REDUCTIONS – the percentage of them is reduced by about half of what it was 1.5 to 2 months ago, from 14% of listings to about 7%. Maybe agents and sellers are pricing correctly now, or maybe they understand that they may spend more than 5 minutes on the market?

Bank owned homes

Another statistic of note are the number of distressed or bank owned properties. We still have fewer than 100 listed out of about 6200 active listings. Less than 1.5%, other markets in the US are not faring as well. People here are still meeting their mortgage payments.

Offer terms that show a big shift

OK – a couple of other things that really stand out to me – the first is that sellers are contributing to buyers closing costs 43% of the time! that’s the highest percentage I can remember seeing. People including appraisal gap language on there offers has almost disappeared (although escalation clauses are still being included) but this makes sense when you see that most sellers are now seeing themselves getting about 99-100% of asking – this number was at 105% or more for a while and that was just crazy. Another option if you are in the previously owned category of home, if you find one you like and it has a motivated seller you could ask for them to do the rate buy down for you. Interest rates have been dipping back down, but it’s doubtful that they will ever get as low as they were during the pandemic. This will likely spur some more buyer activity as we head into spring.

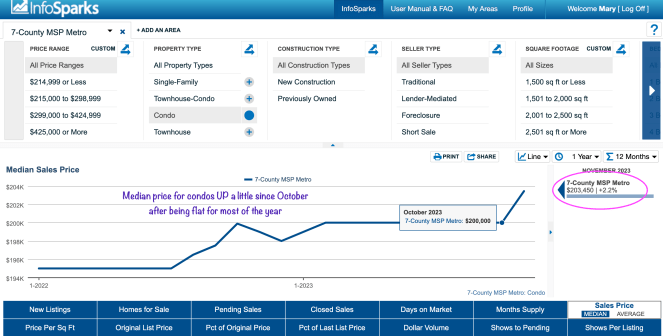

Data on Condos and Townhomes

If you have questions about the real estate market in the Twin Cities area – city or suburbs! – reach out! I love to talk to people that meet me YouTube or the Blog!

Mary

|